Start Date:

03 September, 2025.

End Date:

05 September, 2025.

Course Overview

This training course provides an overview of the ALM (Asset Liability Management) issues through the analysis of its two main components: bank liquidity risk and interest rate risk

Course Objective

To train participants on key components of the ALM and how to take advantage of both the liquidity and interest risks in the market

Course Outline

Structure of bank balance sheet

- Detailed description of asset items, liability items, and off-balance sheet items

- Difference between economic, prudential and accounting management

- Distinction between banking book and trading book

Application: presentation of various banking books (retail bank, capital markets bank)

Fundamental principles of Asset Liability Management

- Aims of ALM : input/output balance

- Modeling the evolution of several assets and liability types : outflow conventions, production hypotheses

- Review of the ALM risk types : liquidity risk, interest rate risk, credit risk, forex risk

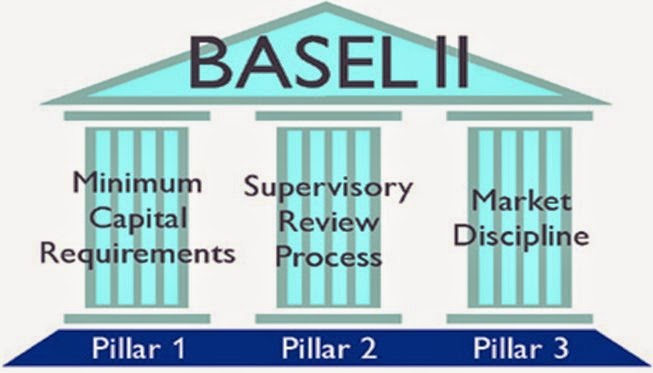

- Factoring in of the ALM risks by the Basel II and IFRS frameworks

- Impact of the current financial crisis and of current evolutions

Assessment of the bank liquidity risk

- Regulatory constraints : liquidity coefficient and observation coefficients

- Determination of the static liquidity gap

- Analysis of liquidity sources and modeling of their mechanisms

- Interaction between liquidity risk, credit risk and market risk

Hedging the liquidity risk

- Hedging short term liquidity risk : REPO operations, securitization

- Optimization and diversification of the refinancing policy in the mid term/ long term

- Implementation of stress tests and simulation of a liquidity crisis : techniques, examples

Definition and impact of interest rate risk

- Definition and measurement scope of bank interest rate risk

- Sources or interest rate risk : displacement or distortion of the yield curve, basis risk, liability and asset-incorporated options, off-balance sheet items

- Assessment of the interest rate risk : fixed interest rate gap and indexed interest rate gap

- Sensitivity of the Net Interest Margin (NIM) and of the balance sheet's Net Present Value (NPV)

Hedging interest rate risk

- Implementation of a limitation system for the general interest rate risk

- Introduction to the Earnings at Risk (EaR) and economic Value at Risk (VaR)

- Implementation of stress tests based on various unfavorable scenarios

- Best practices on the basis of the Basel II committee recommendations